Knowledge is power. And the world today (including financial markets) is constructed in such a way that those with greater intelligence generally have a greater advantage (than those without the knowledge or education) to succeed. The more you learn, the better you can position yourself in life due to your increased awareness.

World-renowned physicist Albert Einstein also knew this. He knew that you need more knowledge before you can get more money. And one of the most profound aspects of money is compound interest.

Einstein once said,

Compound interest is the the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.

Unfortunately, most people today don’t understand the power of compound interest.

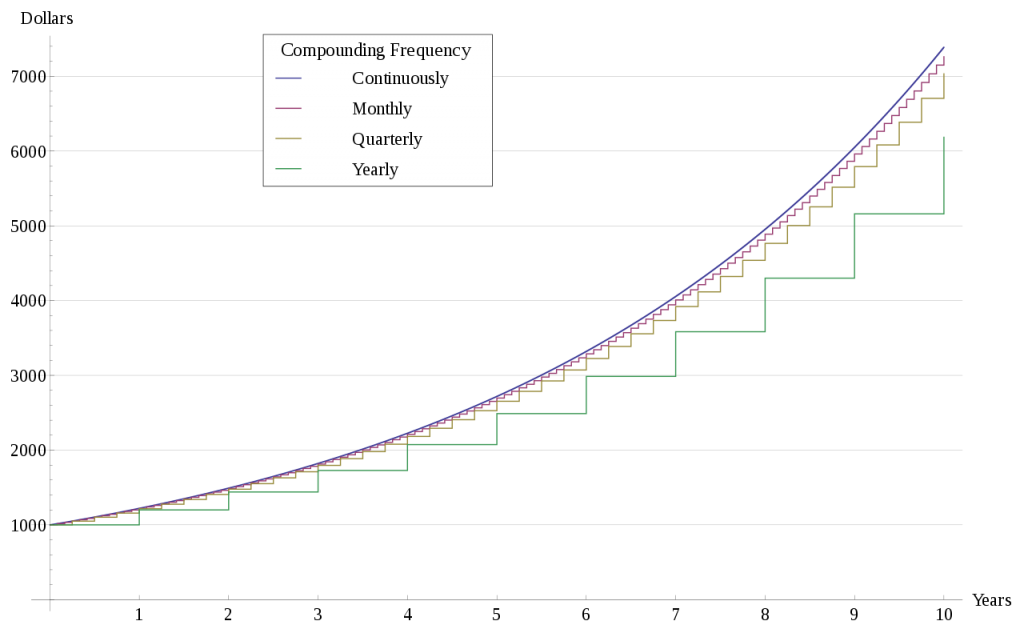

If you accumulated (saved) money, lets say at a rate of $50/week, after 6 months you would have over $1,000 dollars in your bank account. Now imagine if you both accumulated money and it compounded, meaning a small percentage (relative to the total size) was added each month. Then it would grow much faster.

Let’s consider an example.

Which of the two options would you rather have?

A) $1 million dollars right now, or

B) $0.01 cent that doubles every day, for 30 days

Many people would quickly choose option A and run. But option B is actually a better choice.

After just 30 days, option B = $5,368,709.12 !

Clearly, more money comes to those who are patient.

You might be wondering, How can that be? Well the fact is that things which compound, also grow exponentially. Let’s define this to better understand it.

Definition: ex·po·nen·tial growth (noun).

growth whose rate becomes ever more rapid in proportion to the growing total number or size.

Basically, as you begin to accumulate more and more, the size of your investment will keep growing faster and faster if it has any element that compounds. This behavior is actually a mathematical constant.

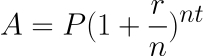

A mathematical formula

Math is nature’s way of saying, “this is truth.” And this is the mathematical formula used to express exponential growth.

A = final amount

P = initial principal balance

r = interest rate

n = number of times interest

applied per time period

t = number of time periods elapsed

You can choose to be on either side of the equation. Either someone who’s earning interest yourself, or someone who’s paying interest to others. But the choice is entirely yours, and it all depends upon how you choose to manage your money.

Most people don’t even bother to try to understand any of this, and it’s no surprise why they are always broke.

What banks do

Banks, credit card companies and money lenders are very aware of compound interest, and they use it every day to make millions of dollars. They call it an Annual Percentage Rate (APR) and this rate is basically a small percentage (in interest) that you pay them every month for buying something today, which you intend to pay off in the future.

APR is very small amounts of money, but when compounded over months and years it adds up to a substantial amount. And when you factor in thousands/millions of customers paying those interest payments, it’s enough to make the banker rich. And this is just one item in their bag of tricks.

So what is the point of all this? If you can understand compound interest, you can use it to your advantage. Instead of always paying interest to your credit cards and loans, you can earn it from them if you never carry a balance.

Take advantage of any opportunity you have to gain compound interest. Learn as much as you can about annual percentage yields, capital gains and dividends. Because if you don’t increase your financial intelligence, someone else who knows more about money will find a way to transfer it from your hand to theirs.

Disclaimer: This article was written for educational and entertainment purposes only. This is NOT financial advice. Always do your own research and please consult with a licensed attorney before making any serious investment. We are not responsible for any investment decisions that you choose to make.